Understanding the taxation of mutual funds is crucial for investors aiming to optimize returns and ensure compliance with Indian tax laws. The Union Budget 2025 introduced significant changes to the tax treatment of mutual funds, impacting both equity and non-equity investments. This guide provides an in-depth overview of the current tax structure for mutual funds in India.

🧾 Taxation Overview for Mutual Funds in 2025

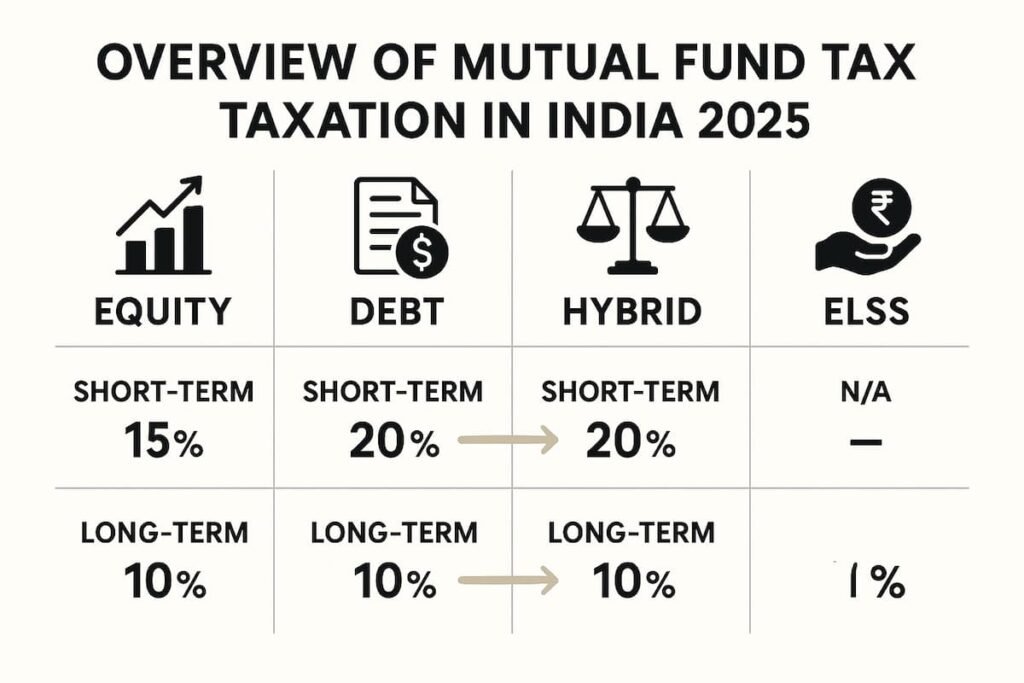

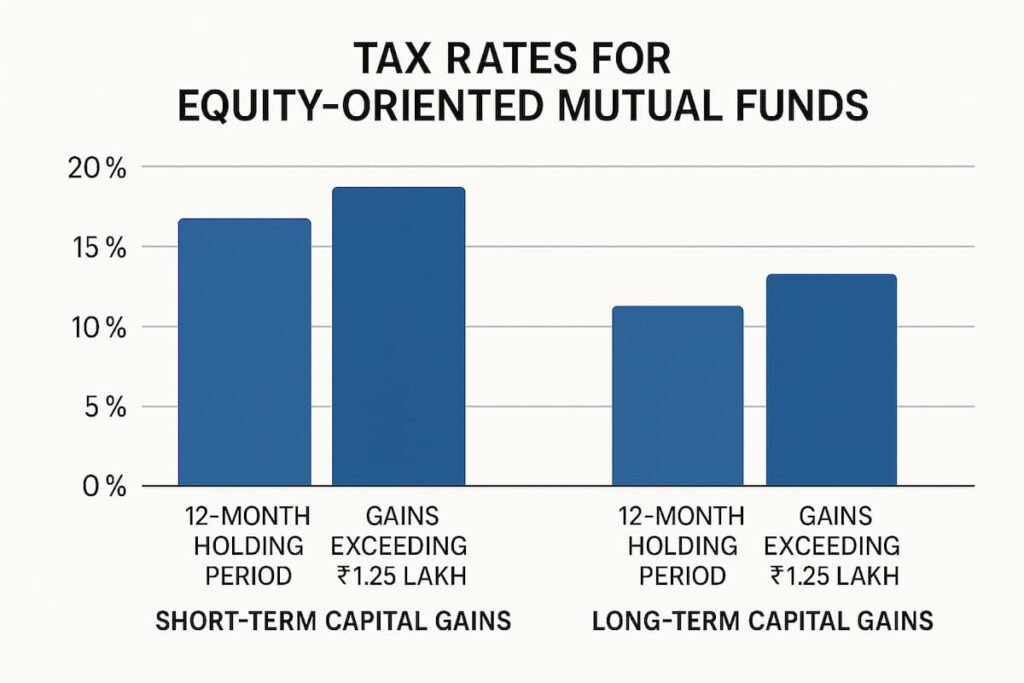

1. Equity-Oriented Mutual Funds

Equity-oriented mutual funds are those that invest at least 65% of their assets in equities. The tax treatment for these funds is as follows:

- Short-Term Capital Gains (STCG): If units are sold within 12 months, gains are taxed at 20%.

- Long-Term Capital Gains (LTCG): For units held beyond 12 months, gains exceeding ₹1.25 lakh are taxed at 12.5%.

These rates apply to both resident and non-resident investors. It’s important to note that the ₹1.25 lakh exemption limit applies to the aggregate of LTCG from all equity-oriented mutual funds in a financial year.

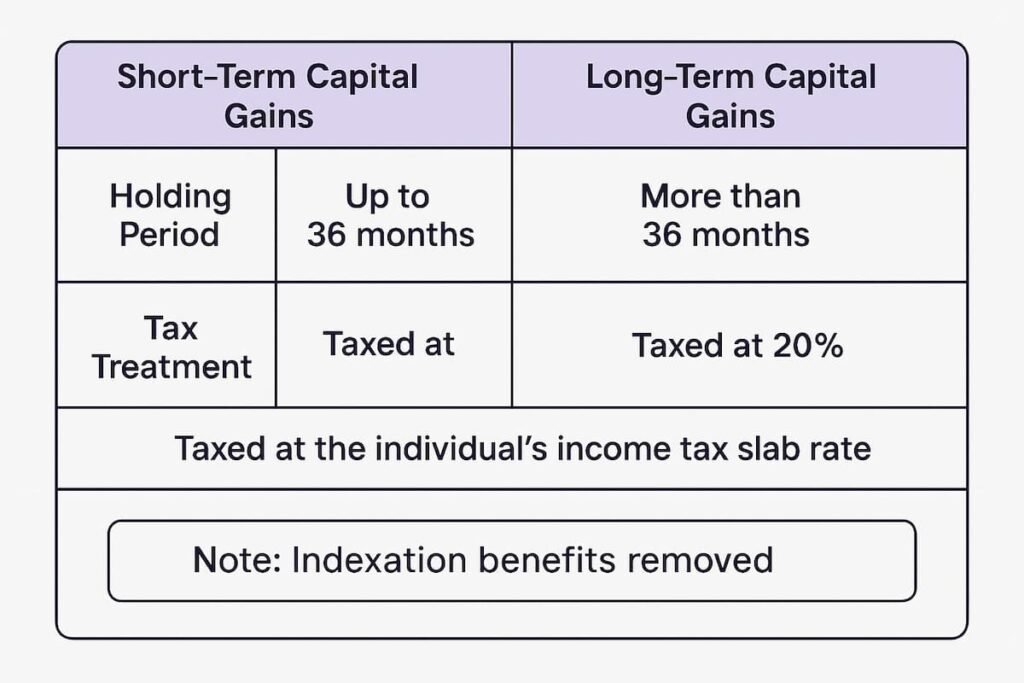

2. Debt-Oriented Mutual Funds

Debt-oriented mutual funds invest primarily in fixed-income securities. The taxation for these funds has undergone changes:

- Short-Term Capital Gains (STCG): If units are sold within 36 months, gains are taxed at the investor’s applicable income tax slab rate.

- Long-Term Capital Gains (LTCG): For units held beyond 36 months, gains are taxed at 12.5% without the benefit of indexation.

These changes align the taxation of debt mutual funds more closely with that of fixed deposits, removing previous indexation benefits.

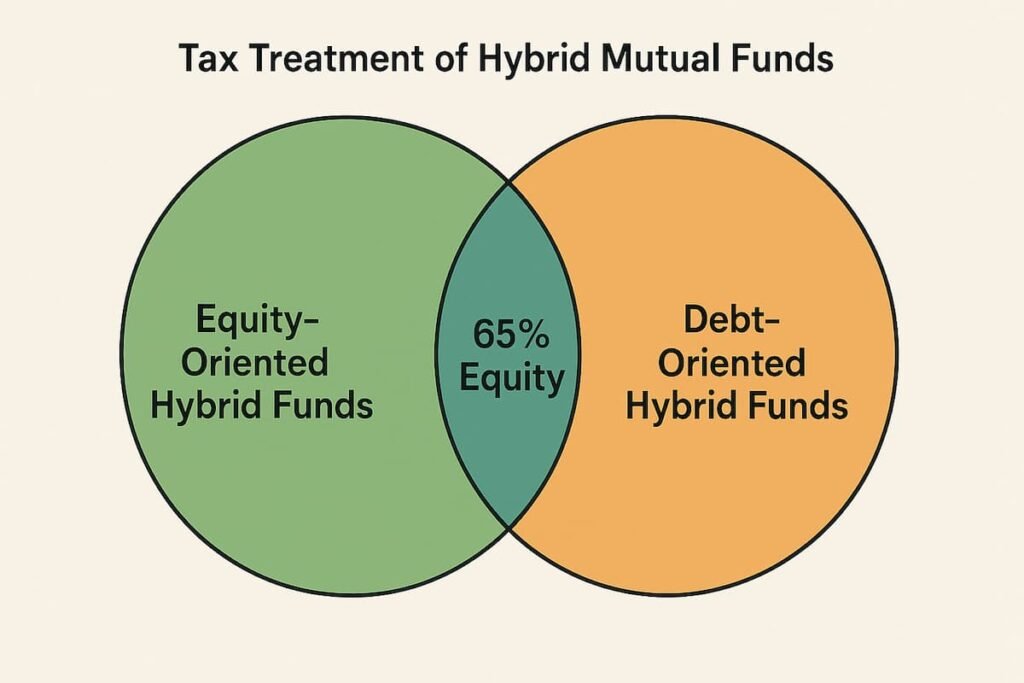

3. Hybrid Mutual Funds

Hybrid funds invest in a mix of equity and debt instruments. The tax treatment depends on the proportion of equity in the fund:

- Equity-Oriented Hybrid Funds: If the equity component is 65% or more, they are taxed as equity-oriented mutual funds.

- Debt-Oriented Hybrid Funds: If the equity component is less than 65%, they are taxed as debt-oriented mutual funds.

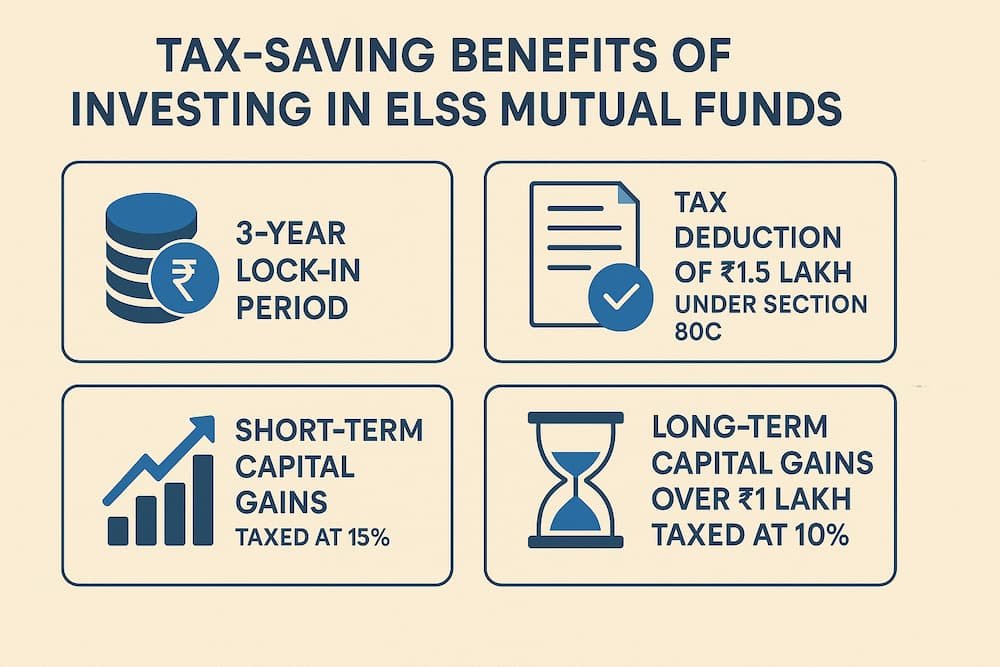

4. Equity Linked Savings Schemes (ELSS)

ELSS funds are equity-oriented mutual funds that offer tax benefits under Section 80C of the Income Tax Act. The tax treatment for ELSS funds is as follows:

- Short-Term Capital Gains (STCG): If units are sold within 3 years, gains are taxed at 20%.

- Long-Term Capital Gains (LTCG): For units held beyond 3 years, gains exceeding ₹1.25 lakh are taxed at 12.5%.

Investors can claim a deduction of up to ₹1.5 lakh per annum under Section 80C by investing in ELSS funds.

5. Dividend Income from Mutual Funds

Dividends received from mutual funds are subject to tax in the hands of the investor. The tax treatment is as follows:

- Resident Investors: Dividends are subject to a 10% Tax Deducted at Source (TDS) if the total dividend income exceeds ₹10,000 in a financial year.

- Non-Resident Investors: TDS is applicable at 20% or as per the applicable Double Taxation Avoidance Agreement (DTAA), whichever is lower.

How to Avoid Taxation on Mutual Funds in India

While it is impossible to avoid taxation altogether, there are strategies to minimize tax liabilities:

- Invest for the Long Term: Long-term capital gains (LTCG) on equity mutual funds are taxed at a lower rate than short-term gains.

- Utilize the ₹1.25 Lakh Exemption Limit: For equity mutual funds, ensure that your long-term capital gains do not exceed ₹1.25 lakh to avoid taxes.

- Invest in Tax-Saving Funds (ELSS): ELSS funds not only provide tax-saving benefits under Section 80C but also have lower taxation rates on long-term gains.

How to Calculate Taxation on Mutual Funds in India

To calculate taxes on mutual funds in India, follow these steps:

- Determine the Holding Period: Check if you held the mutual fund for less than 12 months (short-term) or more than 12 months (long-term) for equity funds, or less than 36 months (short-term) or more for debt funds.

- Calculate Capital Gains:

- Short-Term Capital Gains (STCG): Subtract the cost of investment from the selling price for short-term holdings.

- Long-Term Capital Gains (LTCG): For long-term holdings, subtract the cost of investment from the selling price and apply indexation benefits for debt funds if applicable.

- Apply Tax Rates: Apply the relevant tax rate (20% for short-term equity, 12.5% for long-term equity, income tax slab for debt funds) on the capital gains.

How to Avoid Capital Gains Tax on Mutual Funds in India

It is not entirely possible to avoid capital gains tax, but here are ways to minimize the tax impact:

- Hold for the Long Term: Hold your mutual fund investments for more than a year to benefit from long-term capital gains taxation.

- Use Tax-Advantaged Accounts: Invest in tax-saving funds like ELSS, which offer benefits under Section 80C.

- Offset Capital Losses: If you have incurred capital losses from other investments, you can offset these losses against your capital gains from mutual funds.

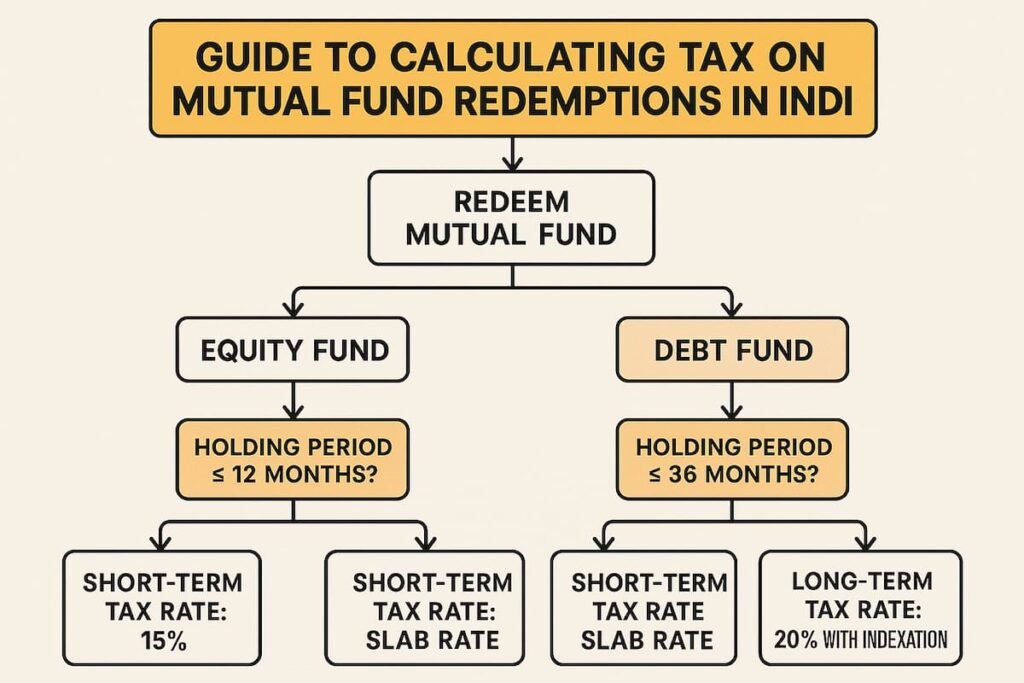

How to Calculate Tax on Mutual Fund Redemption

When redeeming mutual funds, calculate your capital gains as follows:

- Determine the Redemption Amount: Subtract the purchase cost from the redemption value.

- Apply Tax Rate Based on Holding Period:

- For equity funds, if redeemed within 12 months, STCG is applicable, and if redeemed after 12 months, LTCG applies.

- For debt funds, the tax depends on the holding period (within or beyond 36 months).

- Consider Additional Factors: If applicable, apply indexation benefits to long-term debt fund holdings.

🔍 Example Scenarios

1. Retirement Planning

- Investor Profile: A 35-year-old investor aiming to build a retirement corpus over 30 years.

- Recommended Fund: Equity-Oriented Mutual Fund.

- Tax Implications: Long-term capital gains exceeding ₹1.25 lakh will be taxed at 12.5% after 12 months.

2. Short-Term Investment

- Investor Profile: An investor looking to park funds for 2 years.

- Recommended Fund: Debt-Oriented Mutual Fund.

- Tax Implications: Short-term capital gains will be taxed at the investor’s applicable income tax slab rate.

3. Tax Saving

- Investor Profile: An individual seeking tax deductions under Section 80C.

- Recommended Fund: ELSS Fund.

- Tax Implications: Eligible for a deduction of up to ₹1.5 lakh per annum.

🧾 Conclusion

The taxation of mutual funds in India has undergone significant changes in 2025. It’s essential for investors to understand these changes to make informed investment decisions and optimize their tax liabilities. Consulting with a financial advisor can help tailor investment strategies to individual financial goals and tax situations.

📑 FAQ: Frequently Asked Questions about Mutual Fund Taxation in India

1. What is the tax treatment for capital gains from mutual funds in India?

Capital gains from mutual funds are taxed based on the holding period and the type of fund. Short-term capital gains are taxed at higher rates, while long-term capital gains exceeding specified limits are taxed at reduced rates.

2. Are dividends from mutual funds taxable?

Yes, dividends received from mutual funds are subject to tax in the hands of the investor. TDS is applicable if the total dividend income exceeds ₹10,000 in a financial year for resident investors.

3. What are the tax implications for NRIs investing in mutual funds?

Non-Resident Indians are subject to TDS on capital gains and dividend income from mutual funds. The TDS rate varies based on the type of income and applicable tax treaties.

4. How are capital gains from ELSS funds taxed?

ELSS funds are equity-oriented mutual funds with a 3-year lock-in period. Short-term capital gains are taxed at 20%, and long-term capital gains exceeding ₹1.25 lakh are taxed at 12.5%.

5. Can I claim tax deductions for investments in mutual funds?

Yes, investments in ELSS funds qualify for tax deductions under Section 80C of the Income Tax Act, subject to the annual limit of ₹1.5 lakh.

6. What is the impact of the new tax regime on mutual fund taxation?

The new tax regime offers reduced tax rates and does not allow deductions. Investors need to evaluate whether the new regime benefits them more than the old regime, considering their income and deductions.

7. Are there any exemptions available for capital gains from mutual funds?

Exemptions are available for long-term capital gains from equity-oriented mutual funds up to ₹1.25 lakh per annum. No exemptions are available for debt mutual funds.

8. How should I report mutual fund income in my income tax return?

Mutual fund income, including capital gains and dividends, should be reported under the ‘Income from Capital Gains’ and ‘Income from Other Sources’ sections of the income tax return, respectively.