Mutual fund investing remains one of the most effective ways to build wealth over the long term, with its ability to offer both growth and risk management. As we approach the October–December 2025 quarter, investors are increasingly focusing on balanced funds that provide stable returns with manageable volatility. One such fund is the ICICI Prudential Balanced Advantage Fund, which has shown commendable performance over the last few years. This analysis focuses on the 3-year and 5-year performance, highlighting its growth potential, past performance, and predictions for the future.

This fund has a proven track record, with a 3-year CAGR of 14.21% and 5-year CAGR of 15.29%, making it one of the top choices for investors seeking a good mix of risk and returns. In this post, we will take a deep dive into its lump sum and SIP investment performance, analyze potential future returns, and provide recommendations based on different risk levels.

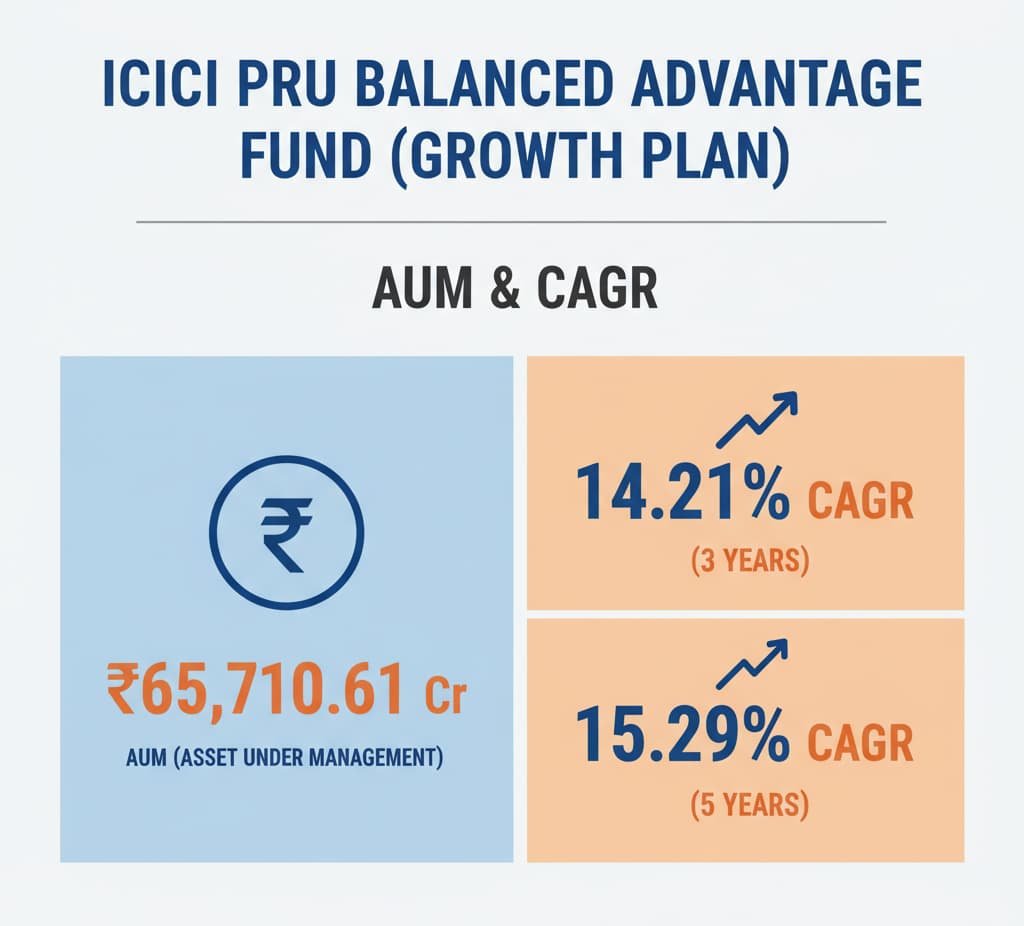

Fund Overview

The ICICI Pru Balanced Advantage Fund (Growth Plan) is a large, well-established fund with an AUM of ₹65,710.61 Cr. Over the past few years, this fund has delivered strong growth, with CAGR of 14.21% over 3 years and 15.29% CAGR over 5 years.

The fund is actively managed by Rajat Chandak and 3 other managers, focusing on a dynamic asset allocation model, which changes the exposure between equity and debt based on market conditions. This flexibility is designed to reduce the overall volatility and enhance returns over the long term. The expense ratio of 0.86% is relatively low, making it an attractive option for investors.

Key Data Summary

- Risk Level: Moderate to Low (Suitable for conservative investors)

- Volatility: 0.43, indicating low volatility, suitable for risk-averse investors.

- Absolute Returns:

- 6-month return: 12.11%

- 1-year return: 7.31%

- 3-month return: 3.34%

This makes it a great choice for investors looking for steady returns with less market risk, especially in the uncertain post-pandemic market environment.

Lump Sum Investment Performance (Past)

For a more practical understanding, let’s see how ₹1 Lakh, ₹5 Lakh, and ₹10 Lakh invested in the fund would have grown over the past 3 and 5 years.

Example 1: Lump Sum Investment for ₹1 Lakh

- If you had invested ₹1 Lakh in October–December 2020 (5 years ago), your investment would have grown to approximately ₹2,01,100 today, based on a CAGR of 15.29%.

- For a 3-year investment, ₹1 Lakh would have grown to ₹1,48,700, using a CAGR of 14.21%.

This shows how a lump sum investment takes advantage of compounding growth over time.

Lump Sum Performance Table

| Investment | 3 Years (Since Oct–Dec 2022) | 5 Years (Since Oct–Dec 2020) |

|---|---|---|

| ₹1,00,000 | ₹1,48,700 | ₹2,01,100 |

| ₹5,00,000 | ₹7,43,500 | ₹10,05,500 |

| ₹10,00,000 | ₹14,87,000 | ₹20,11,000 |

(Calculated using 3Y CAGR = 14.21%, 5Y CAGR = 15.29%)

The table shows the impact of consistent growth over both 3-year and 5-year periods. For larger investments, the compounding effect becomes more pronounced, offering exponential returns.

Lump Sum Investment Predictions (Future)

Now, let’s look at how ₹1 Lakh, ₹5 Lakh, and ₹10 Lakh might perform if invested in the fund in October–December 2025. Based on the CAGR of 14.21% for 3 years and 15.29% for 5 years, here’s what the future could hold:

| Investment | 3 Years (Till 2028) | 5 Years (Till 2030) |

|---|---|---|

| ₹1,00,000 | ₹1,48,700 | ₹2,01,100 |

| ₹5,00,000 | ₹7,43,500 | ₹10,05,500 |

| ₹10,00,000 | ₹14,87,000 | ₹20,11,000 |

This prediction shows that even after 5 years, the fund’s growth rate of 15.29% will lead to significant returns. Investors who make lump-sum investments can take full advantage of long-term growth and compounding.

SIP Investment Performance (Past)

For those looking at Systematic Investment Plans (SIPs), let’s analyze how ₹1,000 and ₹2,000 monthly SIPs would have performed over the past 3 years (starting Oct–Dec 2022) and 5 years (starting Oct–Dec 2020). SIPs spread the investment across time, reducing the impact of market volatility.

Example 2: SIP Investment of ₹1,000 per month

- In 3 years (since Oct–Dec 2022), you would have invested ₹36,000, and the final value would be ₹43,900 based on the historical 3-year CAGR.

- For 5 years (since Oct–Dec 2020), the total investment would have been ₹60,000, with an expected final value of ₹84,500.

SIP Performance Table

| SIP Amount | Total Invested (3Y) | Final Value (3Y) | Total Invested (5Y) | Final Value (5Y) |

|---|---|---|---|---|

| ₹1,000 | ₹36,000 | ₹43,900 | ₹60,000 | ₹84,500 |

| ₹2,000 | ₹72,000 | ₹87,800 | ₹1,20,000 | ₹1,69,000 |

This SIP strategy shows steady growth, with more contributions leading to better growth over the long term. The example clearly demonstrates the power of discipline and consistency in SIP investments.

SIP Investment Predictions (Future)

Here’s how SIPs of ₹1,000 and ₹2,000 per month will grow if started in October–December 2025:

| SIP Amount | Total Invested (3Y) | Expected Value (3Y) | Total Invested (5Y) | Expected Value (5Y) |

|---|---|---|---|---|

| ₹1,000 | ₹36,000 | ₹43,900 | ₹60,000 | ₹84,500 |

| ₹2,000 | ₹72,000 | ₹87,800 | ₹1,20,000 | ₹1,69,000 |

With 15.29% CAGR for 5 years, SIPs will grow consistently, ensuring that investors who commit to regular monthly investments can benefit from the market’s growth over time.

Comparison & Recommendation

- Lump Sum Investment: Best suited for those with lump-sum capital looking to benefit from compounding over the long term. Ideal for investors with a 5-year or longer horizon.

- SIP Investment: Best suited for those who cannot make a large initial investment but want to grow their wealth steadily through regular contributions. It allows averaging of market prices and minimizes timing risks.

Recommendations Based on Risk Level:

- High-Risk Investors: While this fund is not purely equity-focused, it still provides a good balance of growth and stability. If you’re willing to take a higher risk for higher returns, you may want to consider equity-dominant funds.

- Moderate-Risk Investors: This fund is a perfect fit for moderate-risk investors, offering a great balance of equity exposure and debt for stability.

- Conservative Investors: Despite being a balanced fund, its relatively low volatility and consistent returns make it a good choice for conservative investors who are more focused on preserving capital.

Conclusion

The ICICI Pru Balanced Advantage Fund remains one of the top choices for investors in October–December 2025, delivering consistent returns with relatively low risk. Whether you’re considering a lump sum investment or setting up a SIP, the fund provides a flexible and reliable option for different investor types. By considering your risk profile and investment horizon, you can decide the best strategy to grow your wealth in the upcoming quarter and beyond.