In 2025, the insurance industry in India has become increasingly diverse and accessible. With advancements in technology and regulatory improvements, insurance products are designed to meet the specific needs of individuals, families, and businesses. Whether you’re looking to protect your health, your assets, or your family’s future, understanding the various insurance options is essential to make informed decisions.

In this guide, we will delve into the different types of insurance available in India, focusing on life insurance, health insurance, vehicle insurance, and more.

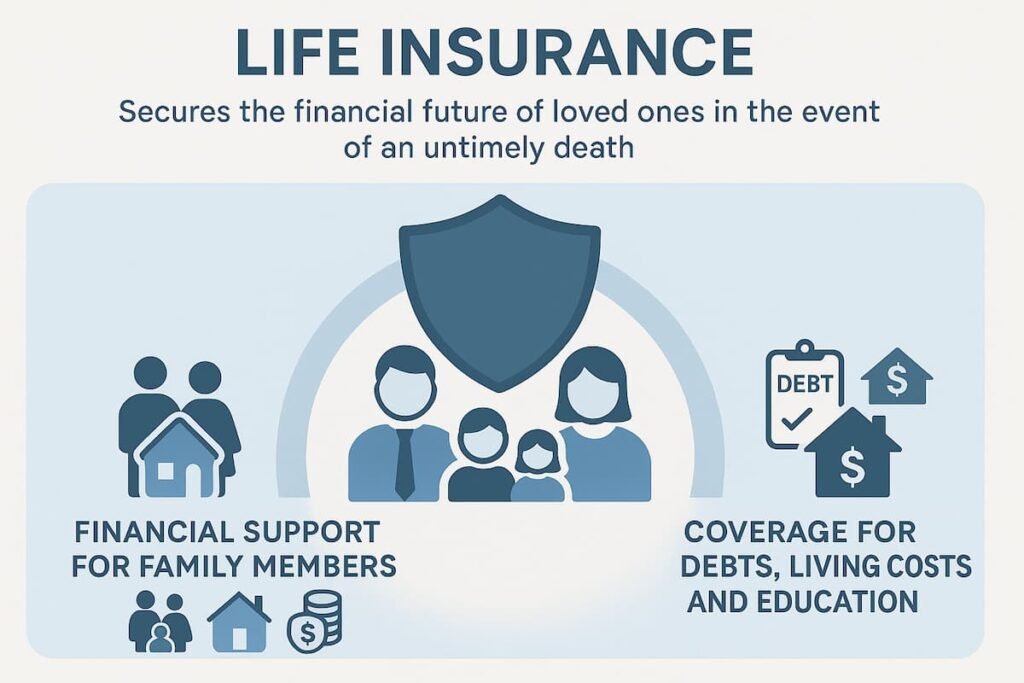

1. Life Insurance

Life insurance is a crucial tool for securing the financial future of your loved ones in the event of your untimely death. It provides a financial cushion for your family, helping them cover expenses such as debts, living costs, and education.

Types of Life Insurance Policies:

- Term Life Insurance

- Description: Term life insurance offers pure protection for a fixed period (e.g., 10, 20, or 30 years). If the policyholder passes away during the term, the beneficiaries receive the sum assured.

- Key Features:

- Affordable premiums.

- No investment or savings component.

- Only provides death benefits, with no maturity benefits.

- Why It Matters: Ideal for individuals seeking high coverage at low premiums. It provides financial security for dependents in case of an unfortunate event.

- Whole Life Insurance

- Description: Whole life insurance offers coverage for the entire lifetime of the policyholder, usually up to 99 or 100 years. It also accumulates cash value over time, which can be accessed or borrowed against.

- Key Features:

- Coverage for life.

- Builds cash value over time.

- More expensive premiums compared to term insurance.

- Why It Matters: Suitable for those looking for lifelong coverage with a built-in savings component.

- Endowment Policies

- Description: Combines life cover with a savings component. The policyholder receives a lump sum amount on the death of the insured or at the end of the policy term (whichever happens first).

- Key Features:

- Provides both life coverage and savings.

- Pays out on death or maturity.

- Premiums are higher than term policies due to the savings element.

- Why It Matters: Useful for those who want to combine protection and savings for future financial goals (e.g., children’s education).

- Money-Back Policies

- Description: These policies provide periodic payouts during the term and a lump sum payout at the end of the policy. It serves both as insurance and an investment plan.

- Key Features:

- Periodic payouts at intervals (e.g., every 5 years).

- Offers both protection and investment returns.

- Why It Matters: Suitable for individuals seeking a mix of insurance protection and income generation during the policy term.

- Unit Linked Insurance Plans (ULIPs)

- Description: ULIPs combine life coverage with investment. A portion of the premium is used for life cover, and the rest is invested in equity or debt instruments.

- Key Features:

- Flexible investment options.

- Dual benefit of insurance and wealth accumulation.

- Investment risks are borne by the policyholder.

- Why It Matters: Ideal for those who want to combine life insurance with potential market returns and are willing to take some investment risks.

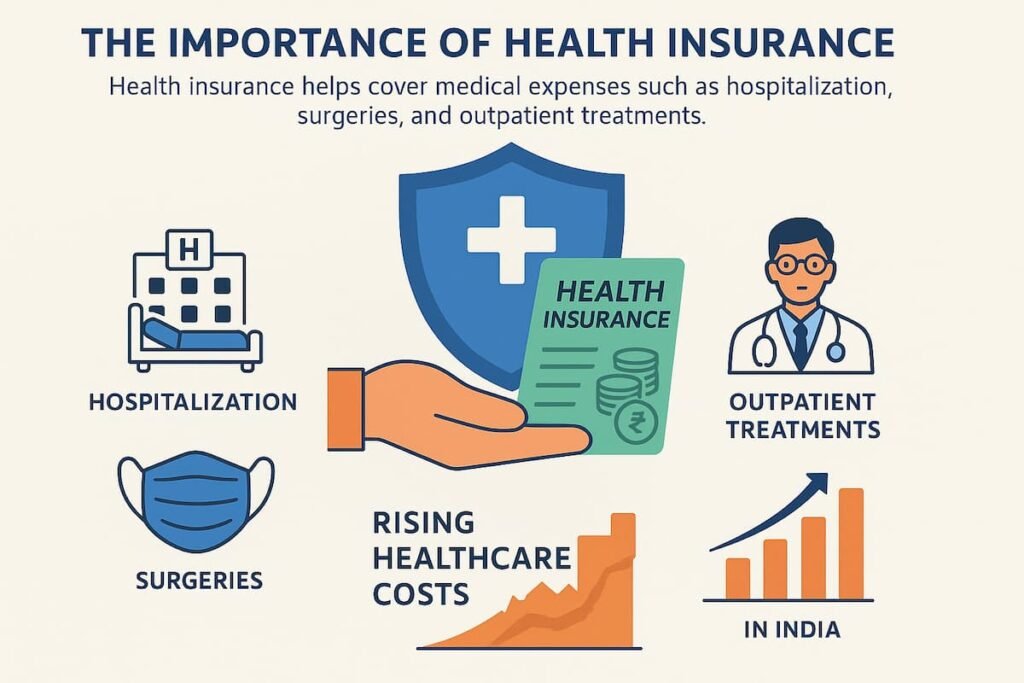

2. Health Insurance

Health insurance helps cover medical expenses, such as hospitalization, surgeries, and outpatient treatments. In a country like India, with rising healthcare costs, having health insurance has become essential for financial protection.

Types of Health Insurance Policies:

- Individual Health Insurance

- Description: Covers the medical expenses of a single individual.

- Key Features:

- Coverage for hospitalization, surgery, and medical tests.

- Cashless hospitalization at network hospitals.

- Why It Matters: Essential for individuals who want dedicated coverage for their medical needs.

- Family Health Insurance (Family Floater Plan)

- Description: This plan covers the entire family under one sum insured. It includes the policyholder, spouse, children, and sometimes dependent parents.

- Key Features:

- Single premium covers all family members.

- Higher sum insured limits than individual plans.

- Why It Matters: Cost-effective solution for families, ensuring everyone is covered for medical emergencies.

- Critical Illness Insurance

- Description: Provides a lump sum payout on the diagnosis of specified critical illnesses like cancer, heart disease, kidney failure, etc.

- Key Features:

- Lump sum payout for serious illnesses.

- Can be bought as a standalone policy or as an add-on to existing health insurance.

- Why It Matters: Crucial for protecting against life-threatening diseases, which often come with high treatment costs.

- Top-Up Plans

- Description: A supplementary plan that offers additional coverage over and above an existing health insurance policy.

- Key Features:

- Lower premiums for added coverage.

- Ideal for individuals who need more coverage than their current policy offers.

- Why It Matters: Provides additional protection without the need for buying a new full-fledged policy.

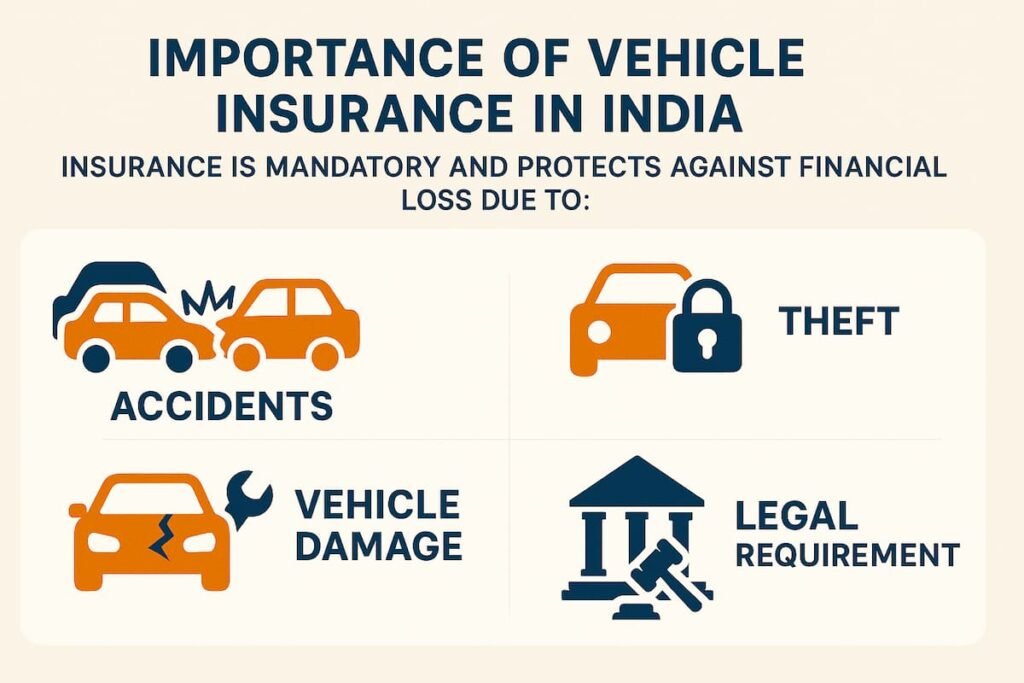

3. Vehicle Insurance

Vehicle insurance is mandatory in India and helps protect against financial loss in case of accidents, theft, or damage to the vehicle.

Types of Vehicle Insurance Policies:

- Car Insurance

- Description: Covers damages to the insured car due to accidents, theft, natural calamities, or fire.

- Key Features:

- Third-party liability coverage (mandatory by law).

- Comprehensive insurance includes damage to own car and third-party coverage.

- Why It Matters: Legally required for vehicle owners and provides financial protection in case of accidents.

- Bike Insurance

- Description: Covers damages to the insured two-wheeler (bike or scooter) due to accidents, theft, or natural disasters.

- Key Features:

- Similar to car insurance, it provides third-party liability and comprehensive coverage options.

- Why It Matters: Mandatory for bike owners and offers protection from financial losses due to unforeseen events.

- Third-Party Liability Insurance

- Description: Covers the legal liabilities arising from accidents caused by the insured vehicle that results in injury, death, or property damage to third parties.

- Key Features:

- Only covers third-party damages, not the insured vehicle.

- Why It Matters: This is the basic, legally required coverage for all vehicles.

- Comprehensive Vehicle Insurance

- Description: Covers both third-party liability and damages to the insured vehicle due to accidents, theft, vandalism, etc.

- Key Features:

- Full protection for the vehicle owner and third parties.

- Why It Matters: Offers extensive coverage, making it a preferred option for vehicle owners.

4. Travel Insurance

Travel insurance provides coverage for unexpected events while traveling, including trip cancellations, medical emergencies, lost baggage, or flight delays.

Types of Travel Insurance:

- Single Trip Travel Insurance

- Description: Covers one specific trip, including medical emergencies, flight cancellations, and lost luggage.

- Key Features:

- Coverage for trip duration.

- Provides emergency medical assistance during travel.

- Why It Matters: Ideal for occasional travelers or those going on one-off vacations.

- Multi-Trip Insurance

- Description: Covers multiple trips within a specified period (usually one year). It is ideal for frequent travelers.

- Key Features:

- Covers multiple trips with a single policy.

- More affordable than buying separate policies for each trip.

- Why It Matters: Cost-effective for those who travel frequently for business or leisure.

- Student Travel Insurance

- Description: Tailored for students studying abroad. Covers medical emergencies, trip cancellations, lost baggage, and more.

- Key Features:

- Covers educational needs like tuition fees and emergency evacuation.

- Why It Matters: Essential for international students who need extra protection during their studies abroad.

Frequently Asked Questions (FAQs)

Q1: What is the difference between life insurance and health insurance?

- Life Insurance: Provides financial protection to your family in case of your untimely death. It ensures that your dependents are financially secure.

- Health Insurance: Covers medical expenses incurred due to illnesses, accidents, and hospitalizations, reducing the financial burden of healthcare costs.

Q2: What is term insurance, and why should I consider it?

Term insurance offers pure life cover for a specified period (e.g., 10, 20, or 30 years). It provides financial protection to your family in case of your death. It is affordable and provides high coverage for low premiums, making it a popular choice for those seeking to protect their family’s future.

Q3: Can I have multiple health insurance policies?

Yes, you can have multiple health insurance policies, either from the same or different insurers. It helps enhance your coverage limits. However, it’s essential to disclose all existing policies when buying a new one to avoid issues during claims.

Q4: What is the difference between comprehensive car insurance and third-party liability insurance?

- Comprehensive Car Insurance: Covers damage to your own car as well as third-party liability, including theft, natural calamities, and accidents.

- Third-Party Liability Insurance: Covers only the damages caused to third parties (injury or property damage) and is legally required in India.

Q5: How does family health insurance work?

Family health insurance covers the medical expenses of the entire family under a single policy. It provides a lump sum or cashless treatment for medical conditions, including hospitalization, surgery, and outpatient services.

Q6: What is the benefit of buying a money-back policy?

A money-back policy provides periodic payouts during the policy term, offering both life coverage and a guaranteed return. This type of policy suits individuals looking for a combination of protection and periodic savings.

Q7: What should I consider when buying car insurance?

Consider the following:

- Coverage: Choose between third-party and comprehensive coverage based on your needs.

- Claim Process: Ensure the insurer has a quick and hassle-free claims process.

- Add-Ons: Check for optional add-ons like zero depreciation, roadside assistance, or engine protection.

Q8: Is term life insurance better than whole life insurance?

Term life insurance is more affordable and provides high coverage for a fixed period. Whole life insurance offers lifelong coverage and builds cash value, but it comes at a higher premium. Your choice depends on your coverage needs and financial goals.

Q9: Can I cancel my health insurance policy after purchasing it?

Yes, most insurers offer a free-look period (usually 15 days) during which you can cancel the policy and get a refund if you are dissatisfied. After the free-look period, cancellation is possible but may involve deductions.

Q10: How does travel insurance help during a trip?

Travel insurance provides coverage for unforeseen events like trip cancellations, medical emergencies, lost baggage, flight delays, and even accidents during your travels. It ensures that you don’t face financial losses while traveling.

Q11: Is medical insurance mandatory in India?

While not mandatory, medical insurance is highly recommended, especially with the rising healthcare costs in India. Many employers provide group health insurance plans, but it is advisable to buy an individual policy for comprehensive coverage.

Q12: What is the benefit of having vehicle insurance in India?

Vehicle insurance is mandatory in India by law and protects you from financial liabilities arising from accidents, theft, and damage to your vehicle. It also ensures that third-party damage caused by your vehicle is covered, avoiding legal issues.

Conclusion

In 2025, the variety of insurance options in India provides individuals and families with flexible and tailored solutions to safeguard their future. From health and life insurance to vehicle and travel insurance, choosing the right insurance policy can help you manage risks and ensure financial stability.

By understanding the different types of insurance and their benefits, you can make well-informed decisions that protect your loved ones, assets, and health. Make sure to evaluate your needs, consider future goals, and seek expert advice to select the best policies for you.