Applying for a credit card in India in 2025 has become more streamlined, thanks to digital advancements and evolving financial products. Whether you’re a first-time applicant or looking to upgrade your existing card, understanding the application process, eligibility criteria, and available options is crucial. This guide provides a comprehensive overview to help you navigate the credit card application journey effectively.

Understanding Credit Cards in India

What is a Credit Card?

A credit card is a financial tool that allows you to borrow funds from a bank or financial institution up to a certain limit to purchase goods or services. You repay the borrowed amount either in full or in installments, with interest applied to outstanding balances. A credit card is not just a payment tool; it can help you build your credit history and access rewards, travel benefits, and other perks.

Types of Credit Cards Available

There are several types of credit cards available in India, each designed to cater to different financial needs and lifestyles. Let’s break them down:

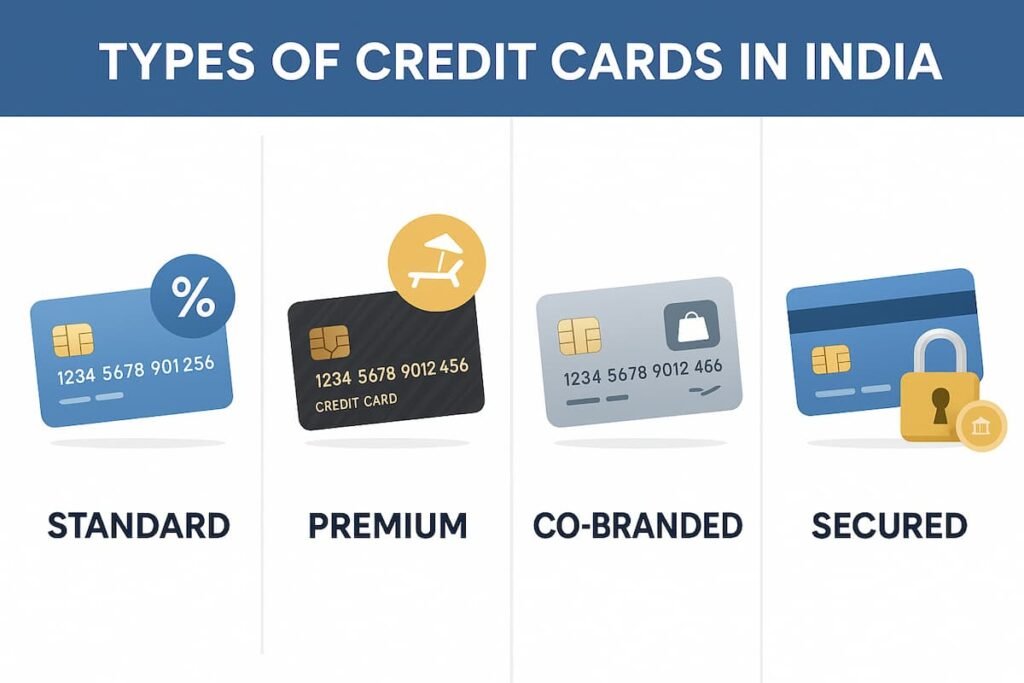

1. Standard Credit Cards

Standard credit cards are the most basic and common types, suitable for general use. They offer essential features such as:

- Low fees compared to premium cards.

- Basic reward programs (such as cashback or points).

- Lower credit limits compared to premium cards.

Eligibility for Standard Credit Cards:

- Minimum income requirement may vary but usually starts from ₹20,000 per month.

- Age: Typically between 18 to 65 years.

- Good credit score (above 650) is preferred.

2. Premium Credit Cards

Premium credit cards provide enhanced benefits for higher-income individuals. These cards are designed for frequent travelers, business professionals, or those who want to enjoy luxurious services and exclusive rewards. Benefits often include:

- Higher credit limits.

- Luxury perks, such as access to airport lounges, concierge services, travel insurance, and more.

- Exclusive rewards like flight miles, cashback, and dining privileges.

Eligibility for Premium Credit Cards:

- Higher income requirement, typically ₹50,000 to ₹1,00,000 per month.

- Age: 21-65 years.

- A strong credit score (750 or above).

- Higher annual fees, but the benefits often outweigh the costs for frequent cardholders.

3. Co-branded Credit Cards

Co-branded cards are issued in collaboration with popular brands, retailers, or airlines. These cards offer specific rewards related to the partnered brand, like discounts on purchases or exclusive services. Examples:

- Airline-specific credit cards offer air miles and benefits like extra baggage allowance or priority check-in.

- Retail co-branded cards offer discounts and special offers at partner stores.

Eligibility for Co-branded Credit Cards:

- Income requirements may vary but generally range from ₹25,000 to ₹60,000 per month, depending on the brand.

- A decent credit score of 700 or higher is often required.

- Age: 18-65 years.

4. Secured Credit Cards

Secured credit cards are designed for individuals who do not have a credit history or have a low credit score. These cards require a security deposit that is often equal to the credit limit, ensuring the issuer’s risk is minimized. Benefits include:

- Easier to obtain for individuals with poor or no credit history.

- Helps in building or rebuilding credit scores.

Eligibility for Secured Credit Cards:

- A fixed deposit, which acts as collateral, is required for the credit limit.

- Income requirements may be lower, often ranging from ₹15,000 to ₹25,000 per month.

- No stringent credit score requirements.

Eligibility Criteria for Credit Card Application

Regardless of the type of credit card you apply for, there are some common eligibility criteria to meet. These may vary slightly depending on the card issuer, but generally, they include:

- Age: Applicants should be between 18 to 65 years of age.

- Income: The required income level will vary based on the type of card you choose. For example, premium cards will have higher income thresholds, while standard and secured cards are more accessible to those with lower incomes.

- Credit Score: A good credit score (750 or above) is preferred, especially for premium and co-branded credit cards. Secured cards and some standard cards may have more lenient credit score requirements.

- Employment Status: Applicants can either be salaried or self-employed, though self-employed applicants may need to provide more documentation (like tax returns).

Before applying, it’s advisable to check the specific eligibility requirements of the credit card you wish to apply for, as some cards may have additional conditions or may offer special benefits based on certain criteria, like age or professional status.

Steps to Apply for a Credit Card in India

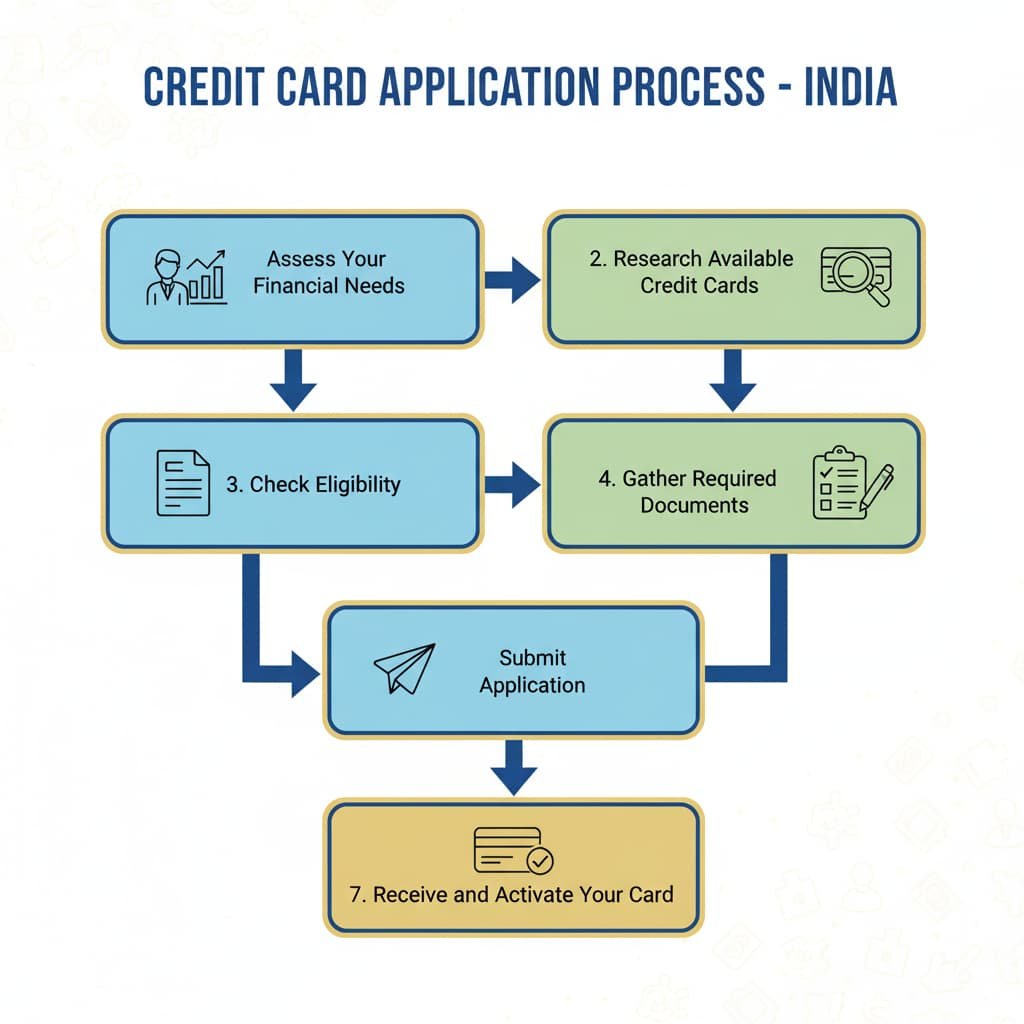

1. Assess Your Financial Needs

Determine the primary purpose of the credit card—be it for shopping, travel, cashback, or building credit history. This assessment will guide you in selecting the most suitable card.

2. Research Available Credit Cards

Explore various credit card options available in the market. Consider factors like annual fees, interest rates, rewards programs, and additional benefits. Comparison websites can provide valuable insights to help you choose the right card.

3. Check Eligibility

Before applying, verify your eligibility for the chosen credit card. This can be done through the issuer’s website or customer service. Some platforms also offer eligibility check tools, making it easier to understand if you’re likely to get approved for the card.

4. Gather Required Documents

Typically, you’ll need:

- Identity Proof: Aadhaar card, PAN card, passport, voter ID, or driving license.

- Address Proof: Utility bills, rental agreement, passport, or bank statements.

- Income Proof: Salary slips, bank statements, or income tax returns.

- Photographs: Recent passport-sized photos.

Requirements may vary by issuer, so be sure to check in advance.

5. Submit Application

Applications can be submitted online through the issuer’s website or mobile app, or offline at the bank’s branch. Online applications are typically processed faster and offer more convenience.

6. Await Approval

The issuer will review your application, verify documents, and assess your creditworthiness. Approval times vary but typically range from a few hours to a few days.

7. Receive and Activate Your Card

Upon approval, the credit card will be dispatched to your registered address. Follow the instructions provided to activate the card. Once activated, you can start using the card for your purchases.

Tips for a Successful Credit Card Application

- Maintain a Good Credit Score: Regularly check and improve your credit score by paying bills on time and reducing outstanding debts.

- Avoid Multiple Applications: Frequent applications can negatively impact your credit score, so be strategic about the cards you apply for.

- Understand Terms and Conditions: Thoroughly read the card’s terms, including interest rates, fees, and reward programs, to avoid any surprises later.

- Use Responsibly: Use your credit card within the limit and make timely payments to avoid penalties and build a positive credit history.

Conclusion

Applying for a credit card in India in 2025 is a straightforward process if you understand the requirements and follow the necessary steps. By assessing your needs, researching available options, and maintaining a good credit profile, you can select a card that aligns with your financial goals and lifestyle. Whether you’re a first-time applicant or looking to upgrade, there’s a credit card option for every need.